?")

")

TVS Motor Company’s International Business Acceleration: Contextual Analysis of the 52% Two-Wheeler Export Surge in November 2025

I. Executive Summary: Decoding the International Momentum

The sales performance of TVS Motor Company in November 2025 represents a critical turning point in the organization’s strategic transition towards global market dominance. The company reported robust aggregate sales of 519,508 units, marking a strong 30% year-on-year (YoY) increase compared to 401,250 units sold in the same month last year.1 Crucially, this overall growth trajectory was not merely volume-driven, but strategically accelerated by the exceptional velocity of its international business segment, which registered its highest-ever monthly export volume.3

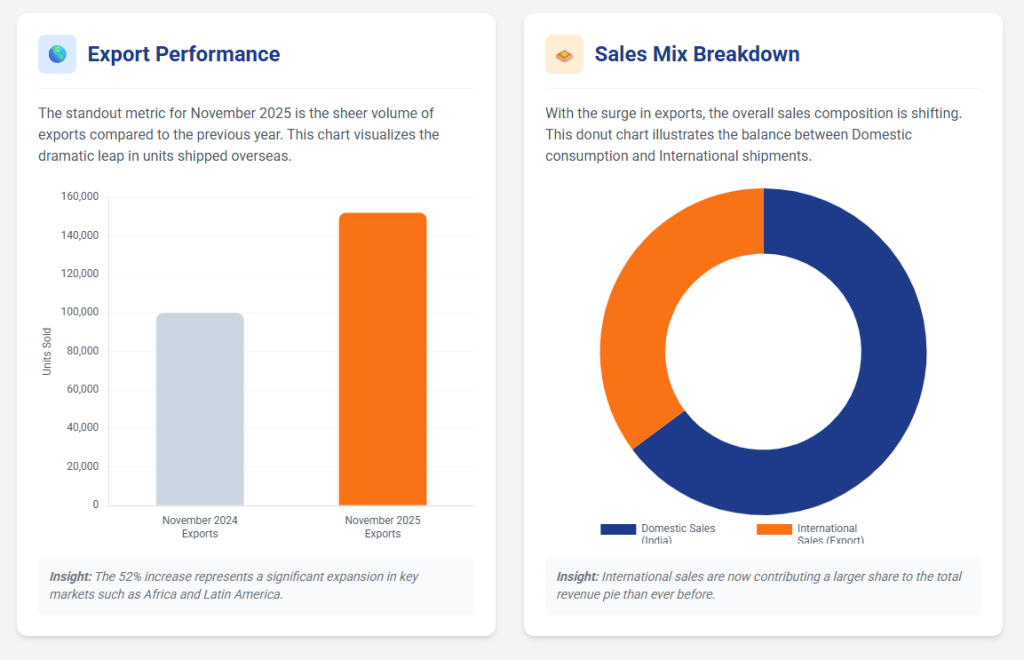

The reported 52% increase in international two-wheeler (2W) sales is the most significant data point from the monthly performance review. This segment delivered 132,233 units in November 2025, up from 87,150 units in November 2024.1 This surge signifies a successful execution of TVS’s long-term global strategy, fundamentally repositioning export markets as the dominant accelerator of the company’s volume and, more importantly, its long-term revenue and margin trajectory.

Five Critical Findings for Strategic Review

Analysis of the comprehensive sales figures confirms that the international momentum provided substantial strategic advantages:

- Primary Growth Accelerator: The total international business registered a 58% growth overall, significantly outpacing the 20% growth seen in domestic two-wheeler sales.1 This dynamic demonstrates a successful strategic de-risking, where export markets are now providing substantial insulation from potential volatility or slower growth in the mature domestic market.

- Portfolio Resilience and Commercial Strength: The international momentum is characterized by breadth and depth, substantiated by an unprecedented 147% surge in the high-utility three-wheeler (3W) segment.2 This rapid increase, driven by a 146.86% rise in 3W exports to 16,082 units 3, validates exceptionally strong commercial mobility demand in key emerging markets and suggests successful tender wins or expansion in urban logistics.

- Competitive Market Share Capture: TVS’s impressive 58% overall export growth contrasts sharply with its key competitor, Bajaj Auto, which reported only 14% global shipment growth for the month.6 This discrepancy indicates that TVS is aggressively and successfully capturing market share, particularly in high-potential emerging market ‘white spaces’ identified in its strategy, such as Latin America.8

- Premium Strategy Validation: The substantial 34% growth in the total motorcycle segment 1, which significantly exceeded the overall 27% growth in total 2W sales, implies a favorable product mix. This momentum suggests that international demand is increasingly weighted toward high-margin premium products (e.g., Apache, Raider), providing direct support for the concurrent improvement in the company’s Q2 FY26 EBITDA margins, which expanded to 12.7%.10

- Long-term Financial Upside and Investor Confidence: The impressive volume surge in November 2025 validates the company’s dual strategy of premiumization and geographical diversification. This reassurance translated immediately into positive investor sentiment, with the TVS stock rising between 3.2% and 3.75% following the sales data release, signaling market recognition of the strengthened growth trajectory.12

II. Quantitative Analysis of November 2025 Sales Performance

The analysis of TVS Motor Company’s November 2025 sales figures reveals a deeply bifurcated growth profile, where international business provides the high-velocity thrust, while the domestic market maintains steady, sizable volumes.

A. Overall Company Sales and Growth Drivers

In November 2025, the company’s total sales reached 519,508 units, representing a 30% increase over the 401,250 units sold in the corresponding period last year.2 Within this total, two-wheelers remained the core volume driver, achieving a 27% increase with sales rising from 392,473 units to 497,841 units.9

A pivotal shift in contribution is evident when comparing domestic and international performance. Domestic two-wheeler sales demonstrated healthy, yet comparatively moderate, growth of 20%, rising from 305,323 units to 365,608 units.1 Conversely, the total international business segment, encompassing both two-wheelers and three-wheelers, surged by 58%, increasing volumes from 93,755 units to 148,315 units.5 This meant that exports constituted 28.5% of the total volume, definitively establishing international markets as the principal accelerator of the company’s overall velocity.

B. Deep Dive: The International Business Portfolio

The focus of this analysis, the international two-wheeler segment, was characterized by a 52% growth rate. In absolute terms, 2W exports increased by 45,083 units, rising from 87,150 units in November 2024 to 132,233 units in November 2025.1 This singular segment generated a substantial portion of the company’s total incremental volume gain of 118,258 units YoY.3

It is essential to view the 52% two-wheeler increase within the context of the 58% total international business growth.5 The differential is largely explained by the exceptional performance of the three-wheeler segment.

The Exponential Rise of the Three-Wheeler Segment

The three-wheeler segment delivered the sharpest rise in the portfolio, with total sales surging by 147%, climbing from 8,777 units to 21,667 units.2 A closer look at the data reveals that exports were the overwhelmingly dominant factor in this segment’s success, with three-wheeler exports rising 146.86% to 16,082 units.3

This extraordinary 3W performance, typically a commercial utility vehicle, strongly suggests successful capture of demand related to infrastructure development or last-mile mobility requirements in emerging economies. Commercial volumes of this magnitude are often more resilient to consumer discretionary spending dips compared to personal 2W sales. Furthermore, these units often contribute favorably to revenue realization. This commercial surge, coupled with the 52% 2W growth, confirms that TVS is executing a comprehensive strategy in emerging markets, capturing both personal and commercial mobility segments simultaneously.

The concentration of growth is clearly illustrated by the breakdown of total export volumes:

Table 1: Contextualizing the 52% Export Growth (Unit Volumes)

| Segment | Nov 2024 (Units) | Nov 2025 (Units) | YoY Growth (%) | Contribution to Total Exports (Nov 2025) |

| International 2W Sales | 87,150 | 132,233 | 52% | 89.15% |

| International 3W Exports (Calculated) | 6,605 | 16,082 | 143.53% | 10.85% |

| Total Exports (Int. Business) | 93,755 | 148,315 | 58% | 100% |

C. Internal Segment Performance Benchmarking

A review of the domestic segments further highlights the importance of the international pivot.

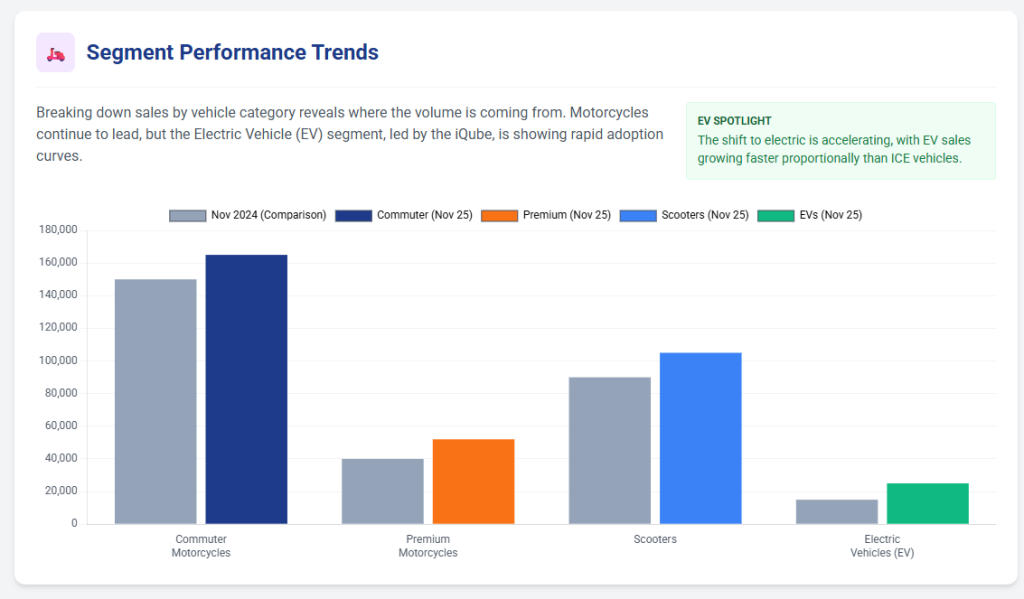

- Motorcycle Segment Dominance: Total motorcycle sales registered a growth of 34%, increasing from 180,247 units last year to 242,222 units in November 2025.1 This growth rate, which surpasses the overall 27% 2W growth, indicates that the motorcycle category—where TVS’s premium and sport models reside—is carrying the highest momentum, suggesting a significant international pull for high-value models.

- Scooter Segment Strength: Scooter sales also exhibited strong performance, growing 27% from 165,535 units to 210,222 units.1

- EV Segment Acceleration: The electric vehicle segment continued its impressive expansion, registering a 46% rise, with sales growing from 26,292 units to 38,307 units.1

This differentiated growth profile, where export 2W and EV units grow in the 40s and 50s while domestic 2W grows at 20%, confirms a deliberate and successful strategic repositioning. By achieving strong growth through higher-velocity international channels, TVS is systematically de-risking the enterprise from potential cyclical downturns or stagnation within the more mature and highly competitive domestic market. The dependence on any single geographical market is substantially diluted by this diversification, which supports high aggregate growth rates required for a company aiming for global scale.

Table 2: TVS Segmental Performance Overview (November 2025 YoY)

| Segment | Nov 2024 (Units) | Nov 2025 (Units) | YoY Growth (%) | Role in Overall Strategy |

| Total Sales (2W + 3W) | 401,250 | 519,508 | 30% | Strong Aggregate Volume |

| Domestic Two-Wheelers | 305,323 | 365,608 | 20% | Steady Domestic Demand |

| International Two-Wheelers | 87,150 | 132,233 | 52% | Primary Growth Accelerator |

| Motorcycles (Total) | 180,247 | 242,222 | 34% | Premiumization & Exports |

| Electric Vehicles (EV) | 26,292 | 38,307 | 46% | Future-Proofing |

III. Competitive Landscape and Market Share Dynamics

The true strategic significance of TVS’s 52% international two-wheeler growth becomes evident only when benchmarked against its primary export-focused competitors, Bajaj Auto and Hero MotoCorp. The data indicates that TVS is gaining considerable traction and challenging the established export hierarchy in the Indian two-wheeler space.

A. Benchmarking Export Velocity (November 2025 YoY)

TVS Motor Company reported a total export growth of 58%, translating to a volume of 148,315 units, achieving its highest-ever monthly export record.3 This performance is strategically superior to the growth rates achieved by key rivals when considering the volume base.

| Table 3: Comparative Global Shipment Growth (November 2025 YoY) |

| OEM |

| TVS Motor Company |

| Bajaj Auto |

| Hero MotoCorp |

B. Assessment of Competitive Dynamics

TVS Outperformance vs. Bajaj Auto

Bajaj Auto, historically recognized as the largest exporter of two-wheelers from India, reported an overall sales growth of 8% in November 2025, with global shipments increasing by only 14% to 2.02 lakh units.6 The substantial disparity between TVS’s 58% growth rate and Bajaj’s 14% growth is strategically critical. This suggests that TVS is effectively challenging Bajaj’s market hegemony in key international markets, likely by exploiting competitive price-points, robust distributor networks, and offering a more technologically current and appealing product mix in regions sensitive to vehicle quality and modernity.

This export velocity gap strongly confirms the successful execution of TVS’s strategy to expand into key emerging market regions that Bajaj traditionally dominated or where new ‘white spaces’ are being rapidly filled. Q2 commentary from TVS specifically highlighted the stabilization of African markets and the identification of LATAM as a major expansion opportunity.8 The massive export surge observed in November 2025 validates that TVS is successfully capitalizing on these opportunities and potentially out-competing its major domestic rival in these critical global territories.

TVS vs. Hero MotoCorp: The Base Effect Analysis

Hero MotoCorp reported a total sales growth of 31%, with its exports jumping by an impressive 70%.17 While Hero’s percentage growth rate is numerically superior to TVS’s 58%, historical analysis suggests that Hero operates off a significantly smaller export base volume compared to TVS and Bajaj. TVS achieved its 58% growth off an already high base volume of 93,755 total units in November 2024.1

The conclusion drawn is that TVS is a sustained, high-volume global player, achieving high growth rates on top of a significant established market presence, whereas Hero’s high percentage growth is more indicative of an aggressive, recent push, possibly benefiting from a lower base from the previous year. The rapid, simultaneous growth demonstrated by both TVS (58%) and Hero (70%) signals a period of intense, escalating competition for global market share among Indian OEMs. While the global market appears receptive, future volume and margin expansion will necessitate persistent investment in product development and international distribution capabilities to maintain this momentum.

IV. Strategic Foundations Driving Global Expansion

The record international sales performance in November 2025 is a direct outcome of TVS Motor Company’s multifaceted strategy centered on premiumization, aggressive geographical expansion, and proactive technological differentiation.

A. Product Mix and Premiumization Strategy

TVS has clearly defined its growth vector through the aggressive push of high-margin premium two-wheeler models, including the Raider, Apache, Ronin, and Jupiter 125/110.8 The fact that total motorcycle sales grew 34%—significantly higher than the overall 27% 2W growth—strongly suggests that these premium models are acting as critical export catalysts. The success of premium exports drives higher profitability, a factor critical for sustaining the recent EBITDA margin improvement. The company has already seen evidence of this, with models like the TVS NTORQ 125 surpassing the 1 lakh sales milestone in international markets.19

Norton Motorcycles and the Global Premium Ambition

Integral to the long-term premiumization strategy is the development of Norton Motorcycles, the company’s UK-based group entity known for its iconic heritage.1 Norton is strategically positioned to serve as TVS’s global premium flagship.8 Commercial production for Norton is scheduled to begin in Q3–Q4 FY26, with full-scale European launches planned for FY27.8 This bold investment enables TVS to penetrate the high-margin, industrialized Western markets, drastically enhancing global brand equity and providing a crucial conduit for high-end technology transfer across the entire TVS platform. This move validates that the current 52% volume surge provides the necessary operational scale and cash flow to finance the R&D and logistical costs of penetrating these capital-intensive premium segments.

B. Geographic Focus and Market Penetration

TVS employs a dual-pronged geographical strategy: solidifying its base in traditional emerging markets while simultaneously targeting new, higher-value regions.

Emerging Market Anchors

The robust volume base in November 2025 is sustained by continued strength in emerging markets, including regions where Africa is stabilizing and markets like Sri Lanka and Nepal are showing improvement.8 The extraordinary 147% surge in 3W exports is highly symptomatic of deep commercial traction in these specific high-volume, commercially intensive emerging economies.3

Exploiting ‘White Space’ and the European Pivot

Latin America has been explicitly identified as a “major white space for market share expansion”.8 The sheer magnitude of the 52% two-wheeler increase strongly indicates that the LATAM market strategy is already yielding significant volumes, accelerating the company’s expansion in a region where two-wheeler penetration is rapidly increasing.

Simultaneously, TVS is executing a strategic pivot toward industrialized markets. Chairman Sudarshan Venu confirmed the company’s intent to enter more European markets, starting with Italy, and expanding to Spain and Portugal.20 This strategy was visibly validated by the company’s debut at EICMA 2025, where it showcased six new products, including the TVS Apache RTX 300, slated for a European launch in Q1 2026.20 This showcase confirms that the strategy goes beyond merely exporting commuter models; it aims to secure future high Average Selling Price (ASP) volumes by catering to the premium, enthusiast segments of developed markets.

C. Operational Leverage and Future-Proofing

TVS’s ability to handle a 58% growth in total exports is a testament to its operational readiness. Achieving its “highest-ever monthly exports” 3 validates the efficiency and capacity utilization across its four manufacturing plants located in India and Indonesia.1 This manufacturing depth provides the essential flexibility to manage the sudden, massive increase in global demand.

Furthermore, the company is proactively preparing for future mobility standards. The electric vehicle portfolio grew 46% 1, with TVS actively expanding its electric 2W lineup (iQube range) and electric 3Ws (King EV Max).8 This demonstrates a commitment to sustainable mobility. While the company has acknowledged short-to- medium-term risks related to magnet availability for EV manufacturing 10, the strategy is proactively addressing this by pursuing alternative sourcing and local partnerships.8 This operational risk management approach is crucial for ensuring the scalability of the EV portfolio, which is paramount for long-term global compliance and maintaining market relevance.

V. Financial Impact and Sustainability Analysis

The record international volume achieved in November 2025 is not just a volume story; it is a critical validation of the company’s financial strategy and its recent strong earnings performance. High export growth is intrinsically linked to improved profitability margins.

A. Quarterly Financial Context (Q2 FY26 Review)

The November performance provides a robust lead-in to the current fiscal quarter (Q3 FY26), reinforcing the financial strength demonstrated in Q2 FY26 (ended September 2025). Q2 FY26 was characterized by TVS achieving its highest-ever quarterly sales, revenue, and profit.11

- Revenue and Profit: Revenue from operations climbed 25.5% YoY to ₹14,051 crore.11 Standalone net profit saw an even higher surge, increasing 36.6% YoY to ₹906 crore.11

- Margin Enhancement: Operating EBITDA grew by a substantial 40% to ₹1,508 crore, with the EBITDA margin improving by 100 basis points, reaching 12.7%.10 This superior margin performance, achieved despite ongoing inflationary pressures in raw material and operational costs, is directly linked to a favorable product and geographical mix—a mix further amplified by the high-margin nature of international sales.

- Q2 Export Momentum: Even before the November surge, Q2 FY26 showed consistent international traction, with two-wheeler exports increasing by 31% to 3.63 lakh units 11, generating revenue from exports totaling ₹2,885 crore.8

Table 4: Key Financial Metrics Comparison (Q2 FY26 vs Q2 FY25)

| Metric | Q2 FY25 (Estimated) | Q2 FY26 | YoY Growth (%) | Significance |

| Revenue from Operations (₹ Cr) | ~11,197 | 14,051 | 25.5% | Record high, validates demand. |

| Standalone Net Profit (₹ Cr) | ~663 | 906 | 36.6% | Strong profit conversion. |

| Operating EBITDA (%) | ~11.7% | 12.7% | 100 bps expansion | Improved product mix, cost control, and favorable exports. |

| International 2W Exports (Units) | ~2.77 Lakh | 3.63 Lakh | 31% | Consistent volume traction in global markets. |

B. Export-Led Margin Improvement and Investor Confidence

The 52% two-wheeler growth in November 2025 functions as a critical component in sustaining and enhancing the 12.7% EBITDA margin achieved in Q2 FY26. Export markets, particularly those being targeted for premium product penetration (like Europe and parts of LATAM), typically yield a higher contribution margin compared to the saturated, price-sensitive domestic commuter segment. This structural shift in the sales mix—from domestically concentrated volume to globally diversified, high-value volume—is fundamental to TVS’s future profitability structure.

The immediate market validation of this performance was strong. Following the release of the November sales figures, the TVS stock demonstrated positive momentum, rising by 3.75% to trade at ₹3,664.00, securing its position as the top gainer in the Nifty Auto index.12 This market reaction underscores the investor community’s recognition that the company is effectively utilizing its volume growth to drive superior financial returns, reinforcing the positive earnings per share (EPS) trajectory, which has grown substantially from ₹213.51 in 2019 to ₹575.19 in 2025.21

Furthermore, the high export volume serves a crucial counter-cyclical function against domestic cost inflation. Raw material costs, for instance, escalated sharply from ₹14,309 crores in 2019 to ₹25,978 crores in 2025.21 Despite these rising operational expenses, the ability to improve the gross profit margin (from 7.65% to 10.88%) is attributed to effective cost management paired with the shift toward higher-margin exports. The 52% growth in international business is thus acting as a necessary margin stabilizer, successfully absorbing domestic inflationary pressures and providing leverage against fluctuating commodity prices.

C. Sustainability Challenges and Financial Risks

While the exponential growth rate is impressive, the focus must now shift to the sustainability of absolute volume gains. The 52% YoY jump may reflect cyclical recovery or seasonal spikes in destination markets, requiring diligent analysis to separate structural, repeatable growth from one-off volume shipments.

A critical consideration for sustainability is the company’s capital structure. TVS Holdings’ total debt has increased sharply, rising from approximately ₹6,991 crores in 2020 to ₹32,488 crores in 2025.21 Although current profitability is robust, this elevated leverage demands continuous generation of high-margin revenue streams, precisely like those produced by the 52% export surge, to ensure comfortable mitigation of risks related to interest obligations and liquidity. The continued expansion into emerging markets, while profitable, introduces inherent risks related to geopolitical instability and local currency depreciation, necessitating enhanced financial risk management and hedging strategies.

VI. Conclusion and Forward-Looking Recommendations

The 52% growth in international two-wheeler sales in November 2025 is definitive proof of TVS Motor Company’s maturation into a formidable global mobility provider. This extraordinary surge is a structural shift, confirming the successful pivot away from a singular focus on the domestic market toward a globally diversified, margin-accretive operational model. The international portfolio is now the primary engine driving aggregate volume and enhancing the overall margin profile, positioning TVS to outperform the industry in the coming fiscal periods.

Synthesis of Strategic Positioning

TVS Motor Company has successfully established a dual strategic structure: a high-volume base sustained by robust demand for commuter and commercial vehicles in emerging markets (Africa, LATAM, validated by the 147% 3W export surge), and a high-value growth trajectory anchored by premium models and the forthcoming entry into industrialized European markets via the Norton platform and models like the Apache RTX 300. This combination of scale and strategic high-value focus is the key competitive differentiator.

Forward-Looking Recommendations

Based on this analysis, the following strategic actions are recommended to capitalize on the international momentum:

- Sustain Aggressive Consolidation in Latin America: The high growth volume confirms successful penetration in LATAM. TVS must now aggressively invest in solidifying local distribution, service networks, and dedicated marketing campaigns to convert initial volume gains into entrenched market share. This consolidation is necessary to proactively counteract inevitable competitive responses from rivals like Bajaj Auto and Hero MotoCorp, whose recent export activity signals escalating global competition.

- Ensure Flawless Execution of European Premium Launches: The upcoming commercial production of Norton and the European market debut of the TVS Apache RTX 300 in Q1 2026 are high-stakes initiatives. Success in these high-standard, high-margin European markets is crucial to elevate global brand perception and secure the planned high Average Selling Price (ASP) revenue stream, which is integral to the long-term margin expansion strategy.

- Enhance Financial Hedging and Risk Mitigation: Given the reliance on international sales for growth and margin stabilization, TVS must increase the sophistication and scope of its financial hedging mechanisms. This is necessary to rigorously protect revenue realization against the heightened risks of currency volatility and economic instability in key African and Latin American emerging economies, ensuring strong volume conversion into stable, domestic-currency profits.

- Capitalize on Commercial Mobility Dominance: The exceptional 147% 3W growth should be leveraged strategically. TVS should accelerate the export expansion of its electric three-wheeler offerings, such as the TVS King Kargo HD EV, into existing and new export territories. This move aligns with global trends toward sustainable urban logistics and allows TVS to capture durable commercial fleet business, further diversifying its revenue mix toward high-utility, resilient segments.

Sources

- TVS Motor November Sales Jump to 5.19 Lakh Units Driven by …, accessed on December 2, 2025, https://www.indiainfoline.com/news/companies/tvs-motor-november-sales-jump-to-5-19-lakh-units-driven-by-motorcycles-scooters-and-evs

- TVS Motor Share Price in Focus; Reports 30% Sales Growth in November 2025 – Angel One, accessed on December 2, 2025, https://www.angelone.in/news/stocks/tvs-motor-share-price-in-focus-reports-30-sales-growth-in-november-2025

- TVS Motor Sales Up 30% in Nov 2025 to 5.19 Lakh Units – Strong Global Demand, accessed on December 2, 2025, https://www.rushlane.com/tvs-motor-sales-up-30-in-nov-2025-to-5-19-lakh-units-12535478.html

- TVS Motor Sales Up 30% in Nov 2025 to 5.19 Lakh Units – Strong Global Demand, accessed on December 2, 2025, https://www.rushlane.com/amp/tvs-motor-sales-up-30-in-nov-2025-to-5-19-lakh-units-12535478.html

- TVS Motor Company sells 5.19 lakh units in Nov’25 | Capital Market News, accessed on December 2, 2025, https://www.business-standard.com/markets/capital-market-news/tvs-motor-company-sells-5-19-lakh-units-in-nov-25-125120100538_1.html

- Bajaj Auto Reports 8% YoY Growth In November 2025 – Domestic Sales Up 3%, Exports Up 14%, accessed on December 2, 2025, https://www.drivespark.com/two-wheelers/2025/bajaj-auto-november-2025-sales-rise-by-8-per-cent-yoy-079599.html

- Bajaj Auto November Sales: Commercial Vehicle Segment Sees Stellar Growth, accessed on December 2, 2025, https://www.ndtvprofit.com/markets/bajaj-auto-november-sales-commercial-vehicle-segment-sees-stellar-growth

- TVS Motor Company Ltd – Profits Growing beyond Expectations, accessed on December 2, 2025, https://simplehai.axisdirect.in/images/2024/TVS-Motors-Ltd—Q2FY26-Result-Update—29102025.pdf

- November Auto Sales 2025 Highlights: Hyundai Motor total sales grow 9.1% to 66,840 units; Maruti Suzuki overall sales rise 26.16% – Upstox, accessed on December 2, 2025, https://upstox.com/news/market-news/stocks/november-auto-sales-2025-live-updates-tata-motors-pv-maruti-suzuki-mahindra-and-mahindra-bajaj-auto-eicher-motors-tvs-hero-moto-corp-share-price/liveblog-185456/

- TVS Motor Reports 37% Profit Surge Amid Record Sales and Revenue – ScanX, accessed on December 2, 2025, https://scanx.trade/stock-market-news/earnings/tvs-motor-reports-37-profit-surge-amid-record-sales-and-revenue/23192957

- TVS Motor Q2 FY26 Results: Record-Breaking Quarter with 42% Profit Growth and 25% Revenue Surge – Torus Digital, accessed on December 2, 2025, https://www.torusdigital.com/toruscope/quarterly-results/tvs-motor-q2-fy26-results-record-breaking-quarter-with-42-profit-growth-and-25-revenue-surge/

- TVS Motor posts strong November as sales jump 20.7%, accessed on December 2, 2025, https://auto.economictimes.indiatimes.com/news/industry/tvs-motor-achieves-207-sales-growth-in-november-2025/125689644

- Nifty Auto Rises as Auto Companies Post Strong November Wholesale Numbers, accessed on December 2, 2025, https://hdfcsky.com/news/nifty-auto-rises-as-auto-companies-post-strong-november-wholesale-numbers

- TVS Motor Company Sales Grows 30 percent in November 2025, accessed on December 2, 2025, https://www.aninews.in/news/business/tvs-motor-company-sales-grows-30-percent-in-november-202520251201165419/

- TVS Motor rises after total monthly sales climb 30% YoY in Nov’25 …, accessed on December 2, 2025, https://www.business-standard.com/markets/capital-market-news/tvs-motor-rises-after-total-monthly-sales-climb-30-yoy-in-nov-25-125120100501_1.html

- TVS Motor posts 30% growth in November, international sales break record, accessed on December 2, 2025, https://www.indiatoday.in/auto/latest-auto-news/story/tvs-motor-posts-30-growth-in-november-international-sales-break-record-2828714-2025-12-01

- Hero MotoCorp achieves 31% growth in November dispatches amid festive demand surge, accessed on December 2, 2025, https://www.livemint.com/auto-news/hero-motocorp-achieves-31-growth-in-november-dispatches-amid-festive-demand-surge-11764605523175.html

- November 2025 Auto Sales HIGHLIGHTS: TMPV exports zoom nearly 33 times, domestic PV sales up 22%; Hero beats forecasts—See how other makers fare – Zee Business, accessed on December 2, 2025, https://www.zeebiz.com/automobile/live-updates-auto-sales-november-2025-live-updates-maruti-suzuki-tata-mahindra-hyundai-honda-bajaj-tvs-hero-bajaj-royal-enfield-eicher-tractor-car-bike-data-384428

- Latest Press Releases – TVS Motor Company, accessed on December 2, 2025, https://www.tvsmotor.com/media/press-release

- TVS Motor Co gearing up for bigger ride in Europe: Chairman Sudarshan Venu – TaxTMI, accessed on December 2, 2025, https://www.taxtmi.com/news?id=61089

- How has been the historical performance of TVS Holdings? – MarketsMojo, accessed on December 2, 2025, https://www.marketsmojo.com/news/stocks-in-action/how-has-been-the-historical-performance-of-tvs-holdings-3734082

Our Social Media Handles

- Instagram : LivingWithGravity

- Medium : Akash Dolas

- YouTube Channel : Gear and Shutter

- Facebook : LivingWithGravity

{kind=link}