?")

Analysis of Piaggio Group’s Strategic Expansion into the Philippines Market

I. Executive Overview: Anchoring Piaggio’s Asia-Pacific Growth Strategy

A. Context and Official Announcement

In a significant move to reinforce its international footprint, the Piaggio Group officially announced the establishment of a new, direct subsidiary in the Philippines during mid-October 2025.1 This decision marks a pivotal strategic transition for the Italian manufacturer, moving away from previous distribution arrangements towards a direct sales operation.1 The expansion is integral to the Group’s long-term goal of penetrating high-potential markets and aligning its mission to deliver premium mobility solutions tailored to the rapidly evolving lifestyles of modern riders across the region.2

The Group’s management views the Philippines as a country of “significant importance” for its international growth strategy.1 The strategic rationale is explicitly centered on tapping into the burgeoning demand for premium European brands in Southeast Asia, a region where the competitive landscape has historically been dominated by high-volume Japanese and Chinese manufacturers.3 By establishing a direct foothold, Piaggio aims to capture a greater share of the value chain and ensure rigorous brand management.

B. Synthesis of Strategic Rationale

The expansion strategy is fundamentally value-driven, targeting consumers with increasing discretionary income who seek distinctive and premium products. The strategy acknowledges the overall market skew towards budget segments but focuses entirely on the high-margin “distinctive premium segments”.1

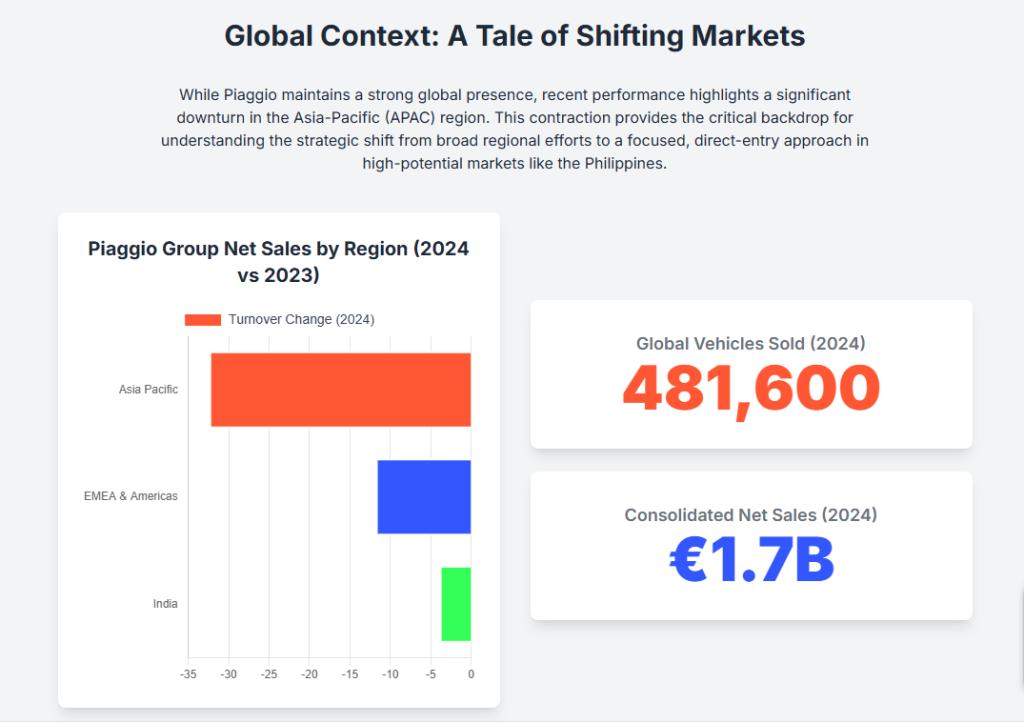

A critical element of this strategic timing is the strong counter-cyclical conviction demonstrated by the Piaggio Group. The expansion is proceeding despite Piaggio facing a “difficult situation on the global markets” and observed market declines in Europe, Asia, and the United States in the first quarter of 2025.1 This approach suggests that the Group identifies the localized macroeconomic trajectory of the Philippines—specifically, the significant rise in income and aspirational spending—as a reliable, high-margin anchor capable of performing independently of current global macroeconomic headwinds.

Furthermore, the shift to a direct subsidiary model is deemed essential for protecting and maximizing brand equity and margin capture. In emerging and competitive markets, reliance on third-party distributors can lead to inconsistent service quality, pricing fragmentation, and potential brand dilution, especially for luxury and lifestyle brands like Vespa and Moto Guzzi. Establishing a direct sales operation guarantees control over service quality, pricing integrity, and enables the deployment of the immersive Motoplex multibrand retail experience, which serves as a crucial differentiator against mass-market rivals.3

C. Operational Scope and Future Diversification

The immediate focus of the new subsidiary is the two-wheeler segment, encompassing a broad premium portfolio:

- Vespa (iconic scooters)

- Piaggio (functional scooters and three-wheelers like the MP3)

- Aprilia (performance scooters and motorcycles)

- Moto Guzzi (high-end classic motorcycles)

The subsidiary will be responsible for the importation and local sale of these vehicles, alongside supplying spare parts and accessories.1 Importantly, the Group has also signaled a potential diversification strategy by confirming that the subsidiary will “explore a possible future interest in the light commercial vehicles market” (LCV).1 This signals an intention to potentially utilize the Piaggio Ape three-wheeled utility vehicle line, a product already widely used across the Asian continent, to capture commercial utility demand in the future.3

II. Philippines Mobility Market: Macroeconomics and Segment Dynamics

A. Market Scale and Regional Importance

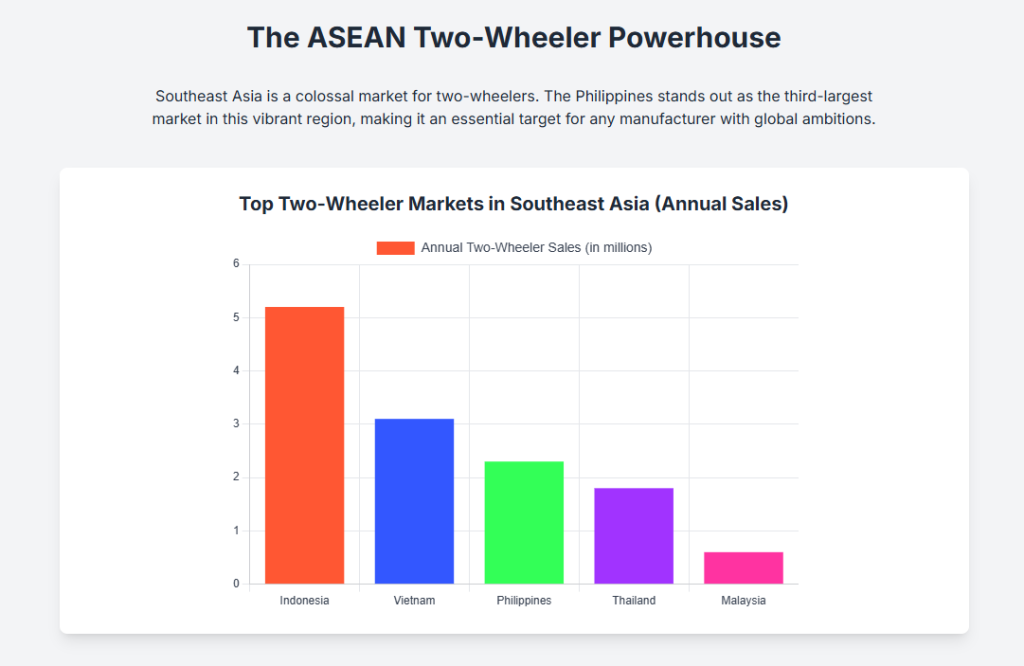

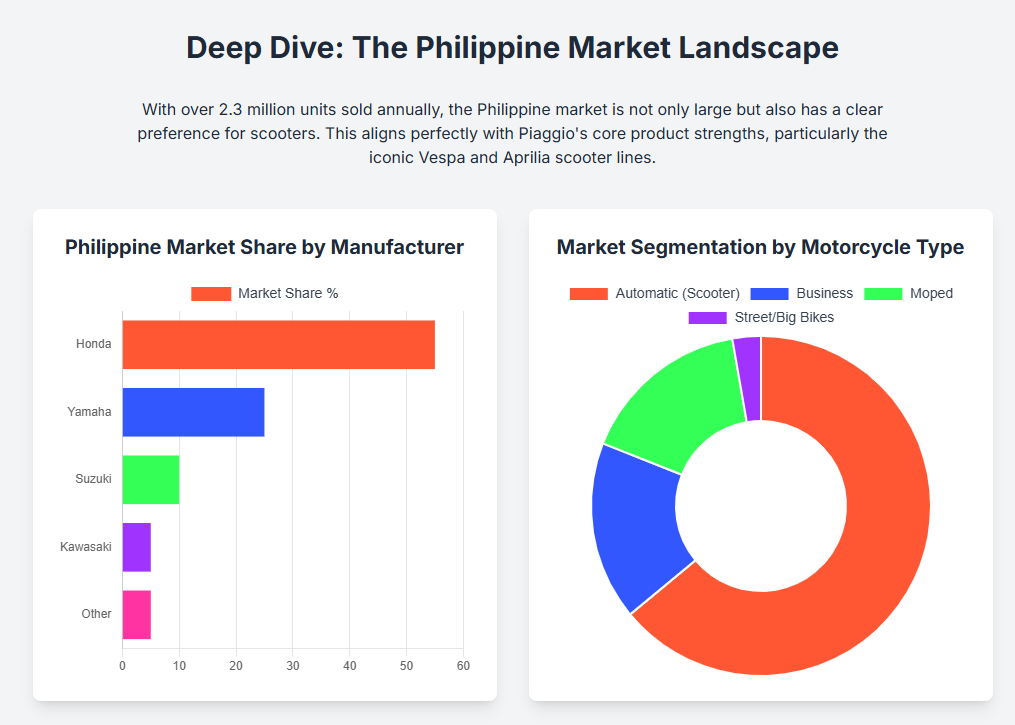

The Philippine two-wheeler market presents an undeniably large addressable volume. The country records annual sales of approximately 2.3 million scooters and motorcycles, with projections suggesting sales could exceed 2.4 million units in 2025.2

This immense volume establishes the Philippines as a critical hub in the Asia Pacific region. It ranks as the third-largest two-wheeler market in Southeast Asia, trailing only Indonesia and Vietnam, and holds the distinguished rank of the fifth-largest two-wheeler market worldwide, behind global giants India and China.2

While the market volume is substantial, the segmentation must be critically understood. The majority of these 2.3 million annual sales are currently concentrated in the commuter and budget segments, which represent the low end of the market.1 Consequently, Piaggio’s strategy is not focused on volume competition but on extracting value from the high-margin niche within this massive consumer base. The Philippine market displays significant resilience, reporting sales up 3.0% and projecting record performance in 2025, even as regional peers like Indonesia and Vietnam experienced slight downturns in the first half of 2024 (-1.0% and -1.4%, respectively).7 This momentum provides a solid foundation for high-CAPEX direct investment.

B. Macroeconomic Tailwinds Justifying Premium Entry

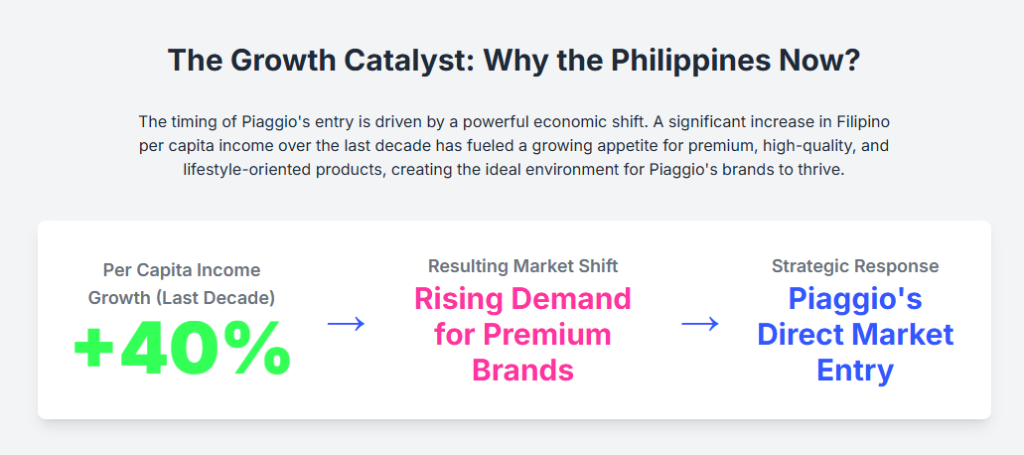

The viability of Piaggio’s premium entry hinges on profound macroeconomic shifts observed over the last decade. Filipino per capita income has experienced remarkable growth, rising by approximately 40%.1 This sustained income uplift has achieved a crucial objective: it has moved a critical mass of consumers past the subsistence level of mobility purchasing, making status and lifestyle a viable motivation for transport expenditure.

This rising prosperity has directly fueled a “growing customer interest in the distinctive premium segments” and generated an observable trend among existing riders to “upgrade to higher-end models”.1 The economic environment now allows discretionary income to be allocated to significantly higher expenditure on transport, validating Piaggio’s decision to time its direct entry at the inflection point where the premium segment graduates from marginal curiosity to a sustainable, high-growth niche.

Urban mobility needs further underscore the market’s structure. Motorcycles serve as the “backbone of daily life” and are the preferred mode of transport due to affordability, fuel efficiency, and the necessity of navigating severe traffic congestion in major metropolitan areas.10 Scooters (the Automatic segment) dominate the overall market, accounting for a commanding 65% of total two-wheeler sales.11 Piaggio’s primary brand, Vespa, is positioned to contest the upper end of this most dominant segment.

| Metric | Value/Ranking (2025) | Strategic Implication for Piaggio |

| Annual Two-Wheeler Sales Volume | ~2.3 Million Units (Projected ~2.4M) 3 | High absolute volume provides fertile ground for niche market extraction. |

| Southeast Asia Market Rank | 3rd (After Indonesia, Vietnam) 2 | Core ASEAN strategic node; complements existing regional manufacturing base. |

| Global Market Rank | 5th (After India, China) 2 | Establishes critical mass for international growth strategy. |

| Per Capita Income Growth (Last Decade) | +40% Increase 1 | Direct financial catalyst enabling the viability of high-margin premium sales. |

| Dominant Segment Share | Automatic/Scooters (65% of market) 12 | Piaggio and Vespa scooters target the high-end of the highest-volume segment. |

III. Piaggio’s Direct Market Intervention and Product Portfolio Strategy

A. Structure and Mandate of the New Subsidiary

The subsidiary has been established as a direct sales operation to secure a “direct foothold” in the market, allowing the Group to control the commercial and customer experience aspects fully.1 The core mandate includes the importation, sale, and distribution of Piaggio Group vehicles, along with the crucial function of supplying spare parts and accessories locally.3

While the official legal name of the new subsidiary has not been publicly identified in the initial announcements 1, the commitment to a direct operational model ensures that Piaggio maintains absolute control over branding, pricing consistency, and quality of service delivery—elements paramount to premium market positioning.

B. The Premium Portfolio Strategy: Vespa, Aprilia, and Moto Guzzi

The new Philippine branch is leveraging the prestige and market recognition of four key brands:

- Vespa: Positioned as the iconic lifestyle scooter, focusing on urban elegance, style, and Italian heritage.2 This brand directly contests the maxi-scooter segment with a luxury angle.

- Piaggio: Covers functional scooter models, such as the innovative three-wheeled MP3.3

- Aprilia: Targets the performance and sport segments, offering high-specification scooters and motorcycles.2

- Moto Guzzi: Anchors the high-end motorcycle offering, targeting the classic, cruiser, and touring niches with significant legacy appeal.1

This portfolio is strategically differentiated from the market incumbents by prioritizing Italian design, innovation, and heritage.2 This approach aims to appeal to consumers who prioritize aesthetic and emotional connection over the sheer utility and value proposition offered by Asian competitors.

A notable structural distinction in the product deployment is how Piaggio is managing brand perception. The primary two-wheeler launch focuses exclusively on these premium and performance brands. Piaggio’s rugged commercial vehicle brand, the three-wheeled Apé, is often managed through a separate commercial vehicles division (Piaggio Vehicles Pvt Ltd, or PVPL) in India.16 By launching the two-wheeler subsidiary first and only exploring LCV interest later, Piaggio avoids immediate brand dilution by preventing the association of the aspirational Vespa and Moto Guzzi brands with utility three-wheelers during the critical initial market entry phase.

C. Integration with Existing APAC Operations and Supply Chain

The expansion into the Philippines is designed to synergize with Piaggio’s already robust manufacturing footprint in Southeast Asia (APAC). The Group operates industrial sites located in Vietnam and Indonesia.9

The Vietnam factory, which opened near Hanoi in 2012, possesses a production capacity of up to 300,000 vehicles per year and is a key supplier of scooters to the wider Southeast Asian markets.17 Additionally, the Group operates a production facility in Cikarang, Indonesia, primarily manufacturing Vespa scooters for the local market, complementing the regional output.19

Since the Philippine subsidiary operates on an import model, it will heavily rely on these regional production bases for efficient logistics and supply stability, likely benefiting from ASEAN regional trade agreements.3 However, this importation model introduces inherent risk in inventory management. The subsidiary must navigate potential currency fluctuations (PHP vs. Euro/USD) and customs delays, which are critical factors when managing sensitive logistics for spare parts and high-specification vehicles, demanding a strategy of maintaining efficient, localized inventory buffers for critical components.

IV. Competitive Landscape and Benchmarking in the Two-Wheeler Sector

A. Dominance of Asian Mass-Market Players

Piaggio enters a market characterized by high concentration and intense volume competition, with Japanese manufacturers maintaining formidable dominance.3 The market leader, Honda, commands a massive 55% market share (selling 945,360 units in FY 2024–2025), and boasts a 67% share within the critical Automatic (scooter) segment.11 Yamaha is the second-place incumbent, demonstrating strong recent growth of 12.7%.11

The majority of consumer demand is centered around small-displacement, high-value models. Top-selling vehicles like the Honda Click, Yamaha Mio, and Yamaha NMAX are predominantly 110cc to 155cc, known for fuel efficiency, reliability, and highly competitive pricing, typically ranging between ₱95,000 and ₱140,000.11

B. Benchmarking Piaggio’s Premium Price Position

Piaggio’s core strategy is to bypass the high-volume, low-margin segments entirely, instead targeting the true luxury tier. The price differential is substantial. For example, a Vespa GTS Super model starts at approximately ₱375,000 in the Philippines.22 This positions the Vespa at roughly three times the price of the highly popular, functional maxi-scooters like the Yamaha NMAX or Honda PCX.

Piaggio’s real competitive arena is therefore not with the mass-market products themselves, but with the high-end variants of existing Japanese models that act as a bridge toward premium mobility. These rivals, such as the Honda PCX and Yamaha NMAX, offer premium features like ABS and larger engine displacements while retaining the Japanese reputation for reliability and supported by extensive dealer networks.11

The growth potential for Piaggio is inherently limited by the elasticity of luxury demand relative to the compelling value offered by these high-quality Japanese alternatives. The market size for a €5,000+ scooter (Vespa) is fundamentally smaller than the enormous market for a €2,000–€3,000 high-specification Japanese maxi-scooter. The Piaggio Group must therefore target the luxury customer driven by status and heritage, rather than the aspirational customer seeking maximum performance and features for their money.

This focused approach, targeting the high-margin niche, also serves to mitigate external financial risks. Although Piaggio’s global sales have shown a downturn (registrations down 15.6% in H1 2025) 6, this decline has been concentrated in global volume markets. By focusing on premium segments in the Philippines, the Group leverages its maintained strong gross margin (30.5% in Q1 2025) 5 per unit sold, effectively insulating profitability from the broader volume competition.

V. Distribution Strategy: Leveraging the Direct Motoplex Model

A. The Motoplex Concept as a Strategic Asset

The distribution strategy centers on the Motoplex concept, Piaggio’s proprietary multibrand retail format.24 Motoplex stores are designed to offer a cohesive, immersive customer experience, integrating the full range of four flagship brands—Piaggio, Vespa, Aprilia, and Moto Guzzi—in a single, unified, lifestyle-oriented space.14 Globally, Piaggio operates 800 Motoplex stores.19

The Motoplex design is critical because it functions as a physical defense mechanism against aggressive digital competition and direct price comparisons. By converting the shopping process into a lifestyle experience emphasizing Italian culture, design, and history, the Motoplex justifies the significant price premium commanded by the Vespa and Moto Guzzi brands over their utility-focused Japanese competitors.2 This experiential approach is difficult for high-volume, transactional brands to replicate.

B. The 3S (Sales, Service, Spares) Imperative

A direct sales operation is essential for maintaining the integrity of the premium offering, particularly concerning after-sales support. The Motoplex structure is specifically engineered to provide comprehensive 3S services (Sales, Service, and Spare Parts) handled directly by professional technicians trained and certified to official Piaggio Group standards.26

For high-performance models like Aprilia and luxury bikes like Moto Guzzi, the quality and authenticity of spare parts and maintenance are non-negotiable elements of ownership. The new subsidiary’s mandate to supply spare parts and accessories locally 3 is vital for reducing wait times, ensuring authenticity, and mitigating the risks associated with grey market servicing, thereby protecting the vehicle’s long-term residual value and the customer experience.

C. Network Rollout and Scaling

Piaggio has previous experience in the Philippine market, having opened a Motoplex store in Manila as early as 2016.25 The establishment of the new direct subsidiary in 2025 provides the foundation to fully control and scale this strategy rapidly.

The Group’s strategy, demonstrated in other dynamic markets like Indonesia (Jakarta, Bali, Surabaya) 14, dictates a targeted approach. Initial expansion will concentrate on the National Capital Region (NCR) and other major urban centers (e.g., Cebu, Davao) where the concentration of rising income levels and demand for lifestyle mobility solutions is highest. The internalization of distribution suggests that Piaggio concluded that maximizing growth and brand control necessitated the termination or shift in reliance on previous, indirect dealer partners.

VI. Future Growth Horizon: Light Commercial Vehicles (LCV) and Electrification

A. The Strategic Option for Apé LCVs

Beyond the two-wheeler portfolio, the new subsidiary’s charter includes the exploration of a “possible future interest in the light commercial vehicles market”.1 This is a strategic acknowledgment of the immense utility market in the Philippines, where Piaggio produces its long-running, three-wheeled Apé brand.3 LCVs fulfill a crucial last-mile logistics and commercial transportation requirement in densely populated and congested urban environments.27

B. Synergy with Existing Electric 3-Wheeler Operations

Piaggio already possesses an established pathway into this segment, primarily via its electric three-wheeler models. In 2023, Piaggio Vehicles Pvt Ltd (PVPL), the Indian subsidiary, pioneered the launch of the electric Apé (Apé E-City and Apé E-Xtra models) in the Philippines through a local partner.16

A core technological differentiator is the utilization of SUN Mobility’s advanced battery-swapping technology in these Apé Electrik vehicles.16 This innovation addresses one of the major barriers to EV adoption—range anxiety and charging downtime—making the Apé Electrik a viable, high-uptime commercial asset. The Apé Electrik was launched as the Philippines’ “first electric three-wheeler,” aligning directly with the government’s ambitious targets for significant EV adoption by 2030.28

The LCV segment represents a strategic hedging mechanism for the Piaggio Group, diversifying its potential revenue base away from purely discretionary lifestyle spending toward utility-driven commercial demand. If the premium scooter market were to face an economic downturn or saturation, the stable, high-volume demand for commercial Apé transport, capitalizing on urbanization and delivery service growth, offers a consistent revenue stream.

C. LCV Integration and Competitive Landscape

The electric two- and three-wheeler (LEV) market is competitively fragmented, featuring domestic and international manufacturers such as NWOW, Tojo Motors, and BEMAC.30 However, Piaggio’s existing partnership model, which includes manufacturing in India and utilizing SUN Mobility’s battery-swapping system, provides an established, differentiated offering that addresses infrastructural limitations more effectively than conventional plug-in charging models.16

The establishment of the direct two-wheeler subsidiary in 2025 creates the operational foundation for potentially integrating the Apé LCV operations. Internalizing the Apé business, currently managed by a local partner, would allow for centralized brand management, logistics optimization, and full control over the highly strategic battery-swapping ecosystem partnership, leading to greater economies of scale and control over the utility segment.

VII. Strategic Challenges and Risk Mitigation

A. Competitive and Financial Risks

The primary competitive risk for Piaggio stems from the high volume and cost-effectiveness of incumbent Asian OEMs. These competitors continually deploy technological innovations and streamlined cost structures to offer products at highly competitive prices, posing a threat to the Group’s economic viability if the premium value proposition is not strictly maintained.32 Despite the noted increase in per capita income, the Philippine market remains “Highly Price-Sensitive”.33 Piaggio must aggressively counter the challenge of “high initial cost” for premium vehicles through superior branding and service quality.34

Furthermore, the Group is exposed to global financial headwinds. Despite the local focus, Piaggio is still managing significant market declines elsewhere and must execute costly transitions to comply with stricter environmental standards, such as Euro 5 plus vehicles.5

B. Operational and Regulatory Hurdles

Operationally, the Philippines presents several non-market-specific challenges that affect all imported goods and services:

- Infrastructure: Severe infrastructure gaps, including crippling traffic congestion in Metro Manila and challenges related to port congestion, directly complicate logistics for vehicle delivery and spare parts distribution.33

- Regulatory Environment: The country’s bureaucratic and regulatory system is complex, with noted challenges including graft, corruption, and cumbersome procedures for permits and product registration.33

- Intellectual Property (IP) Risk: As with many emerging markets, Piaggio faces elevated risks concerning IP infringement or design plagiarism, which could undermine the technological and design advantage that forms the core of its premium positioning.35

C. Mitigation Strategies and Nuanced Market Realities

Piaggio’s choice of an import-only strategy for its core two-wheeler business is a form of political risk mitigation. By avoiding local manufacturing, the Group limits the high capital expenditure and regulatory friction associated with setting up a full-scale plant in a market cited for governance challenges.33

The strategic importance of the Motoplex structure cannot be overstated in this context; it is the Group’s primary tool for enforcing premium pricing, standardizing the luxury experience, and mitigating the competitive threat from high-volume rivals.25 Direct control over the supply chain, leveraging established APAC hubs in Vietnam and Indonesia, is essential for stabilizing logistics and parts availability.9

A significant market contradiction exists regarding Piaggio’s performance brands (Aprilia and Moto Guzzi). While these vehicles are designed for open-road performance, the immediate market utility in metropolitan areas is centered on navigating congestion.33 This suggests that the highest volume of sales for these performance motorcycles will not be driven by daily commuting but rather by leisure and weekend touring, necessitating a geographically targeted distribution strategy focused on affluent residential and ex-urban markets, rather than dense commercial districts.

VIII. Conclusion and Actionable Recommendations

A. Strategic Conclusion

The establishment of a direct Piaggio subsidiary in the Philippines in 2025 is a calculated, structurally sound strategic move that appropriately positions the Group to exploit the convergence of high market volume and surging disposable income in the premium segment. This move, executed despite global financial headwinds, underscores a long-term conviction in the unique demographic trajectory of the Philippines. By internalizing distribution control, Piaggio can safeguard its high-margin revenue streams and enforce the integrity of its Italian luxury brands—Vespa, Aprilia, and Moto Guzzi—against aggressive Japanese incumbents. The future exploration of the LCV segment via the electric Apé further provides a critical layer of commercial diversification.

B. Competitive Benchmarking Summary

| OEM/Segment | Strategic Focus | Key Product Examples | Estimated Price Range (PHP) | Piaggio’s Competitive Response |

| Japanese Mass/Bridge | Reliability, Volume, Value | Honda PCX, Yamaha NMAX 11 | ₱95,000 – ₱140,000 11 | Superior design, heritage, and exclusivity (Motoplex experience) to justify the price multiplier. |

| Piaggio (Scooters) | Lifestyle, Heritage, Premium Margin | Vespa GTS, Piaggio MP3 22 | Starting at ₱375,000 (GTS Super) 22 | Direct control over branding and service to ensure premium value delivery. |

| Piaggio (Motorcycles) | Performance, Touring, Niche | Aprilia, Moto Guzzi 3 | Above ₱400,000 22 | Compete purely on performance and brand legacy against high-end Japanese and specialty imports. |

| LCV Utility/EV | Commercial, Last-mile Logistics | Apé Electrik (E-City, E-Xtra) 16 | N/A (Highly variable by configuration) | Leverage Indian manufacturing base and strategic differentiation through battery-swapping technology. |

C. Actionable Recommendations

Based on this analysis, the following actions are recommended for Piaggio Group management to maximize the success of the new direct subsidiary:

- Accelerate Motoplex Rollout in Affluent Corridors: Immediate priority must be placed on securing prime retail and service locations within the National Capital Region (NCR) and key secondary cities (e.g., Cebu, Davao). The experiential retail element is non-negotiable for justifying the premium price point; therefore, rapid deployment and stringent staff training on the 3S standards are critical to differentiating the Piaggio Group experience from the mass market.

- Define and Execute LCV Integration Pathway: Management should formalize a definitive timeline and mechanism for transitioning the existing Apé Electrik operations, including the strategic SUN Mobility battery-swapping partnership, from the current PVPL/partner structure into the new direct subsidiary. Centralizing control over the utility segment maximizes operational efficiency, ensures technological coherence, and secures the Group’s position as a leader in electric commercial three-wheelers in the Philippines.

- Implement Targeted Marketing for Intangible Value: The subsidiary must strictly maintain its avoidance of mid-range price competition. Marketing and communications must be laser-focused exclusively on the intangible value proposition: Italian heritage, design exclusivity, and lifestyle affinity. The primary objective is not to compete with the Honda Click commuter, but to convert owners of sophisticated Japanese maxi-scooters (NMAX/PCX) who are ready for a status upgrade into Vespa or Aprilia buyers. This requires an emphasis on the product as a form of cultural expression rather than pure utilitarian transport.

Sources

- The Piaggio Group bolsters its presence in the Asia Pacific region with the establishment of a new subsidiary in the Philippines, accessed on October 20, 2025, https://www.piaggiogroup.com/en/archive/press-releases/piaggio-group-bolsters-its-presence-asia-pacific-region-establishment-new

- Piaggio Group Strengthens Asia Pacific Presence with New Subsidiary in the Philippines, accessed on October 20, 2025, https://news.imotorbike.com/en/2025/10/piaggio-group-strengthens-asia-pacific-presence-with-new-subsidiary-in-the-philippines/

- Piaggio Group sets up new Philippines subsidiary as premium bikes grow | Visordown, accessed on October 20, 2025, https://www.visordown.com/news/piaggio-group-sets-new-philippines-subsidiary-premium-bikes-grow

- the piaggio group bolsters its presence in the asia pacific region with the establishment of a new subsidiary in the philippines, accessed on October 20, 2025, https://wide.piaggiogroup.com/en/articles/markets/the-piaggio-group-bolsters-its-presence-in-the-asia-pacific-region/index.html

- Earnings call transcript: Piaggio Group faces market challenges in Q1 2025, accessed on October 20, 2025, https://uk.investing.com/news/transcripts/earnings-call-transcript-piaggio-group-faces-market-challenges-in-q1-2025-93CH-4078384

- Piaggio 2025. Global Sales Tumble Down in Double-Digit During the First Half, accessed on October 20, 2025, https://www.motorcyclesdata.com/2025/09/06/piaggio/

- ASEAN Motorcycles – Facts & Data 2025 | MotorCyclesData, accessed on October 20, 2025, https://www.motorcyclesdata.com/2025/08/22/asean-motorcycles-industry/

- Segment Y Automotive Intelligence: Piaggio expands in ASEAN with new Philippine subsidiary, accessed on October 20, 2025, https://www.segmenty.com/

- Download pdf – Piaggio Group, accessed on October 20, 2025, https://www.piaggiogroup.com/sites/default/files/documents/Semestrale%202024%20ENG%20pubblicato%209%20agosto.pdf

- The Philippines Buys So Many Motorcycles, It’s Ridiculous – RideApart.com, accessed on October 20, 2025, https://www.rideapart.com/features/756599/500k-new-motorcycles-philippines-q1-2025/

- Best Selling Motorcycles in Philippines 2025: Top Models & Market Trends – Accio, accessed on October 20, 2025, https://www.accio.com/business/best_selling_motorcycle_in_philippines

- HPI Solidifies Its No. 1 Position in the Philippine Motorcycle Market for April 2024 – March 2025 | Honda PH, accessed on October 20, 2025, https://www.hondaph.com/news/hpi-solidifies-its-no-1-position-in-the-philippine-motorcycle-market-for-april-2024-march-2025

- Piaggio Group in the Philippines: Vespa and Aprilia land in one of Asia’s major markets, accessed on October 20, 2025, https://moto.motorionline.com/en/The-Piaggio-Group-in-the-Philippines–Vespa-and-Aprilia-land-in-one-of-the-main-Asian-markets./

- PT Piaggio Indonesia Expands Its Premium Network with the 19th Motoplex 4-Brand Dealer, Now in South Jakarta’s Lifestyle Hub to Provide Convenient Access to Premium Vehicles – News & Exclusive Offer | Aprilia, accessed on October 20, 2025, https://aprilia.co.id/en/news/detail/pt-piaggio-indonesia-expands-its-premium-network-with-the-19th-motoplex-4-brand-dealer-now-in-south-jakarta-s-lifestyle-hub-to-p

- Piaggio Group: Homepage, accessed on October 20, 2025, https://www.piaggiogroup.com/en

- Piaggio Vehicles Brings Its Electric Three-Wheeler To Philippines – Motoring Trends, accessed on October 20, 2025, https://motoring-trends.com/alternative-energy/piaggio-vehicles-brings-its-electric-three-wheeler-to-philippines

- Piaggio Group: official opening of new Vietnam factory, accessed on October 20, 2025, https://www.piaggiogroup.com/en/archive/press-releases/piaggio-group-official-opening-new-vietnam-factory

- PIAGGIO VIETNAM WON TWO ASIA AWARDS – Vespa.com, accessed on October 20, 2025, https://www.vespa.com/vn_EN/vespa-world/news/piaggio-vietnam-won-two-asia-awards/

- The Piaggio Group bolsters presence in Asia Pacific with the …, accessed on October 20, 2025, https://www.piaggiogroup.com/en/archive/press-releases/piaggio-group-bolsters-presence-asia-pacific-opening-new-production-facility

- Philippines 2025. Motorcycles Market Scored the Best First Half Ever with 1.2 Million Sales, accessed on October 20, 2025, https://www.motorcyclesdata.com/2025/07/29/philippines-motorcycles/

- 2025 Best Seller Motorcycles in Philippines: Top Models & Market Trends – Accio, accessed on October 20, 2025, https://www.accio.com/t-v1/business/best-seller-motorcycle-in-the-philippines

- Best Motorcycles Below Above ₱400000 in Philippines 2025 – Zigwheels, accessed on October 20, 2025, https://www.zigwheels.ph/new-motorcycles/above-400000

- Scooter Motorcycles Philippines, New Scooter Motor Price 2025 & Specs – Zigwheels, accessed on October 20, 2025, https://www.zigwheels.ph/new-motorcycles/best-scooter

- PIAGGIO GROUP:, accessed on October 20, 2025, https://www.piaggiogroup.com/sites/default/files/documents/PIAGGIO%20-%20Info%20di%20background%20FY2025_ING.pdf

- Piaggio Group expands distribution network on indian and APAC market, 12 motoplex stores opened in India, Vietnam, Indonesia, China, Japan and Philippines in past few month, accessed on October 20, 2025, https://www.piaggiogroup.com/en/archive/press-releases/piaggio-group-expands-distribution-network-indian-and-apac-market-12

- PT Piaggio Indonesia Opens the First Motoplex 4 Brand in Kalimantan, further expanding the service – Aprilia, accessed on October 20, 2025, https://aprilia.co.id/en/news/detail/pt-piaggio-indonesia-opens-the-first-motoplex-4-brand-in-kalimantan-further-expanding-the-service

- Trends in other light-duty electric vehicles – Global EV Outlook 2024 – Analysis – IEA, accessed on October 20, 2025, https://www.iea.org/reports/global-ev-outlook-2024/trends-in-other-light-duty-electric-vehicles

- partnership piaggio vehicles pioneers 3-wheeler electric mobility in philippines through india-made ape’ electrik, introduces swappalble ev solutions – Wide Magazine, accessed on October 20, 2025, https://wide.piaggiogroup.com/en/articles/markets/piaggio-vehicles-pioneers-3wheeler-electric-mobility-in-philippines/index.html

- Driving the EV Revolution in the Philippines. – Kadence, accessed on October 20, 2025, https://kadence.com/driving-the-electric-vehicle-revolution-in-the-philippines/

- Philippines Light Electric Vehicle Market Outlook to 2027 – Ken Research, accessed on October 20, 2025, https://www.kenresearch.com/industry-reports/philippines-light-electric-vehicle-market

- Philippines Electric Three-Wheeler Market Size & Share | Growth Forecast Report 2030, accessed on October 20, 2025, https://www.vynzresearch.com/automotive-transportation/philippines-electric-three-wheeler-market

- Annual Report 2023 – Piaggio Group, accessed on October 20, 2025, https://www.piaggiogroup.com/sites/default/files/documents/Piaggio%20Group%20Annual%20Report%202023%2017%20April.pdf

- Philippines – Market Challenges – International Trade Administration, accessed on October 20, 2025, https://www.trade.gov/country-commercial-guides/philippines-market-challenges

- Philippines Electric Two-Wheeler Market Size & Share | 2030 – VynZ Research, accessed on October 20, 2025, https://www.vynzresearch.com/automotive-transportation/philippines-electric-two-wheeler-market

- PIAGGIO S.p.A. – CFA Institute, accessed on October 20, 2025, https://www.cfainstitute.org/sites/default/files/-/media/documents/support/research-challenge/challenge/rc-2011-winning-rpt-politecnico-di-milano.pdf

Our Social Media Handles

- Instagram : LivingWithGravity

- Medium : Akash Dolas

- YouTube Channel : Gear and Shutter

- Facebook : LivingWithGravity

?")

{kind=link}

{kind=link}